Robo-advisors have been around for years. Betterment, one of the oldest, was founded over ten years ago in 2008 and has $29 billion in assets under management (as of April 2021). It still pales in comparison to Vanguard, founded in 1975 and has $7.2 trillion in assets under management (as of January 2021), but it has carved out a sizable niche in the investing world.

I think robo-advisors are a great innovation. I just don’t use one.

For me, I suspect it’s an issue of timing. I started investing in 1998 with a nascent Roth IRA my dad helped me open with Vanguard.

My “real” start to investing wouldn’t come until I graduated from college and started working in 2003. That was a full five years before any robo-advisors existed.

By the time they started, I was no longer in their target market. I’d done the research and the up-front work, I was already invested at the allocations I wanted, and I was focused on saving more.

That said, as I look back, I don’t know if I’d have invested with a robo-advisor if they were around when I started.

Here are a few of the reasons why:

Table of Contents

- I Want to Do It Myself

- What Got You Here, Won’t Get You There

- 6.8% Betterment Account #1 (70% Stocks, 30% Bonds)

- Betterment Account #2 (90% Stocks, 10% Bonds)

- Personal Capital (70% Stocks, 17% Bonds, 13% Alternatives)

- Target Date Fund Alternatives

- Underlying Strategy Changes

- Costs & Fees Matter

- Many Don’t Offer a Plan

- Final Thoughts

I Want to Do It Myself

When you’re young, you have more time than money.

When I was younger, if something broke, I’d try to fix everything myself. Sometimes, even today, I will try to fix things myself if it’s possible and I have the time because there’s a sense of pride involved. Just recently, our HVAC’s outdoor unit stopped working and I was able to fix it by replacing the capacitor. It turns out that that’s the only thing you can fix without a license in those things, but it was a fun point of pride.

Before kids, I’d study things for hours because I had hours to study them. Now, not so much.

But back then, I learned about investing by reading. Whether it was books or websites, I read a lot. And I knew enough to know that investing didn’t have to be fancy or complicated to work.

I chose a few inexpensive options in my 401(k) and supplemented it with index funds in my Roth IRA and taxable accounts. I didn’t have a financial plan, but I knew that I needed to save for retirement, so I saved.

I don’t think I would’ve needed a robo-advisor to help me do any of that because I wanted to do it myself. That’s not to say DIY is better (and it often isn’t!) But knowing my nature, chances are I wouldn’t have wanted to pay any fee to someone to help me do it.

What Got You Here, Won’t Get You There

“What got you here, won’t get you there” is an idea I’ve seen pop up in a lot of areas of my life.

When you’re younger, it’s important to fit in with the group, follow the rules, and listen to your teachers. As you get older, success is often a function of your ability to think outside of the box, be creative, and recognizing that the rules are merely guidelines. 🙂

The same idea holds in many areas, including investing.

In investing, the key early on is to save as much as you can and get your money into the market. What you pick is important but not as important as saving a lot.

As you age, it’s about getting your allocation right and taking on an adequate level of risk for your needs. Saving more, while good, is less important because your nest egg is so large. Diversifying risk, rebalancing, and other tasks take on greater importance. When you’re nearing retirement, you better make sure your allocation doesn’t have as much risk as a 20-year-old!

For new investors, robo-advisors help by taking away the scary step of picking what to invest in. When you don’t have to worry about the “right” allocation or the “right” investments, you can focus on saving money and getting it into your account.

That’s a huge positive and has resulted in a lot more savings than would otherwise happen.

That said, the challenge will present itself as you transition into the middle game of investing.

The trouble with robo-advisors is that they invest in a whole lot of things. Just check out this 35-year-old’s portfolio at Betterment and Personal Capital:

6.8% Betterment Account #1 (70% Stocks, 30% Bonds)

38% Goldman Sachs Active Beta US Large-Cap (GSLC) (Fee 0.09%)

1.1% Vanguard Small Cap ETF (VB) (Fee 0.05%)

9.8% iShares Core MSCI EAFE ETF (IEFA) (Fee 0.09%)

11.7% Goldman Sachs Emerging Markets Equity (GEM) (Fee 0.37%)

9.6% iShares MSCI EAFE Small Cap ETF (SCZ) (Fee 0.33%)

0.5% iShares TIP ETF (TIP) (Fee 0.20%)

3.0% Goldman Sachs Treasury Access ETF (GBIL) (Fee 0.12%)

9.9% Vanguard Long Term Corporate Bond (VCLT) ( Fee 0.07%)

0.8% Goldman Sachs Access Investment Grade Corporate ETF (GIGB) (Fee 0.14%)

2.4% Goldman Sachs Access High Yield Corporate Bond (GHYB) (Fee 0.34%)

5.7% iShares Emerging Markets USD Bond ETF (EMB) (Fee 0.40%)

7.2% Market Vectors JP Morgan EM Local Currency Bond (EMLC) (Fee 0.30%)

Betterment Account #2 (90% Stocks, 10% Bonds)

32.3% Vanguard Total Stock Market ETF (VTI) (Fee 0.04%)

8.3% Vanguard Value ETF (VTV) (Fee 0.05%)

7.0% Vanguard Mid-Cap Value ETF (VOE) (Fee 0.07%)

5.9% iShares Russell 2000 Value ETF (IWN) (Fee 0.24%)

22.9% Schwab International Equity ETF (SCHF) (Fee 0.06%)

13.9% Vanguard FTSE Emerging Markets (VWO) (Fee 0.14%)

0.6% Vanguard Short Term Inflation Protected Securities ETF (VTIP) (Fee 0.06%)

1.1% iShares Core Total US Bond Market ETF (AGG) (Fee 0.05%)

3.7% iShares National AMT-Free Muni Bond ETF (MUB) (Fee 0.07%)

2.8% Vanguard Total International Bond ETF (BNDX) (Fee 0.09%)

1.5% iShares Emerging Markets USD Bond ETF (EMB) (Fee 0.40%)

Personal Capital (70% Stocks, 17% Bonds, 13% Alternatives)

2.2% iShares Gold Trust ETF (IAU) (Fee 0.25%)

0.8% iShares Intl Treasury Bond ETF (IGOV) (Fee 0.12%)

2.5% Vanguard Global ex-US Real Estate Index ETF (VNQI) (Fee 0.14%)

4.9% Vanguard Tax-Exempt Bond Index Fund ETF (VTEB) (Fee 0.08%)

1.7% iShares iBoxx $ Investment Grade Corporation (LQD) (Fee 0.35%)

3.8% Vanguard REIT Index Fund ETF (VNQ) (Fee 0.12%)

2.0% iShares TIP Bond ETF (TIP) (Fee 0.19%)

0.8% Vanguard Total Bond Index ETF (BNDX) (Fee 0.09%)

2.3% iShares 3-7 Yr Treasury Bond ETF (IEI) (Fee 0.15%)

0.8% iShares 0-5 yr TIPS Bond ETF (STIP) (Fee 0.06%)

3.4% Vanguard Short Term Bond Index Fund EGTF (BSV) (Fee 0 .07%)

6.5% iShares Russell 2000 ETF (IWM) (Fee 0.19%)

13.6% Schwab International Equity ETF (SCHF) (Fee 0.06%)

2.7% Schwab US Small-Cap ETF (SCHA) (Fee 0.05%)

1.6% Vanguard Small-Cap Value Index Fund ETF (VBR) (Fee 0.07%)

1.9% Vanguard FTSE All-World ex US Small Cap ETF (VSS) (Fee 0.12%)

1.8% PowerShares DB Optimum Yield Diversified ETF (PDBC) (Fee 0.58%)

0.11% iShares 0-5 Yr High Yield Corporate Bond (SHYG) (Fee 0.30%)

5.8% Vanguard FTSE Emerging Markets Index Fund (VMO)

OMG.

It’s great that he was invested. That is, by far, the most important factor in a successful portfolio.

But what happens when he ventures into the middle game, where investors often gain the confidence to pick their investments? We learn that it’s not nearly as scary as it once was, and you can get quite a bit of performance just investing in a simple three or four-fund portfolio. You don’t need the laundry list of investments.

The trouble is when you want to transition to a simpler portfolio. Getting from that list to a three to four-fund portfolio will have some pain associated with it and could be a deterrent.

You could argue that you can skip this messy transition period and save yourself some headaches by going with a simple portfolio from the start.

One alternative to a full-on roboadvisor is to work with something like Vanguard’s Personal Advisor – their advisors recommend an asset allocation based on your financial needs but it’s solely Vanguard funds and it’s like a handful, not a dozen+. Also, they have a Vanguard Digital Advisor that is very similar to robo-advisors.

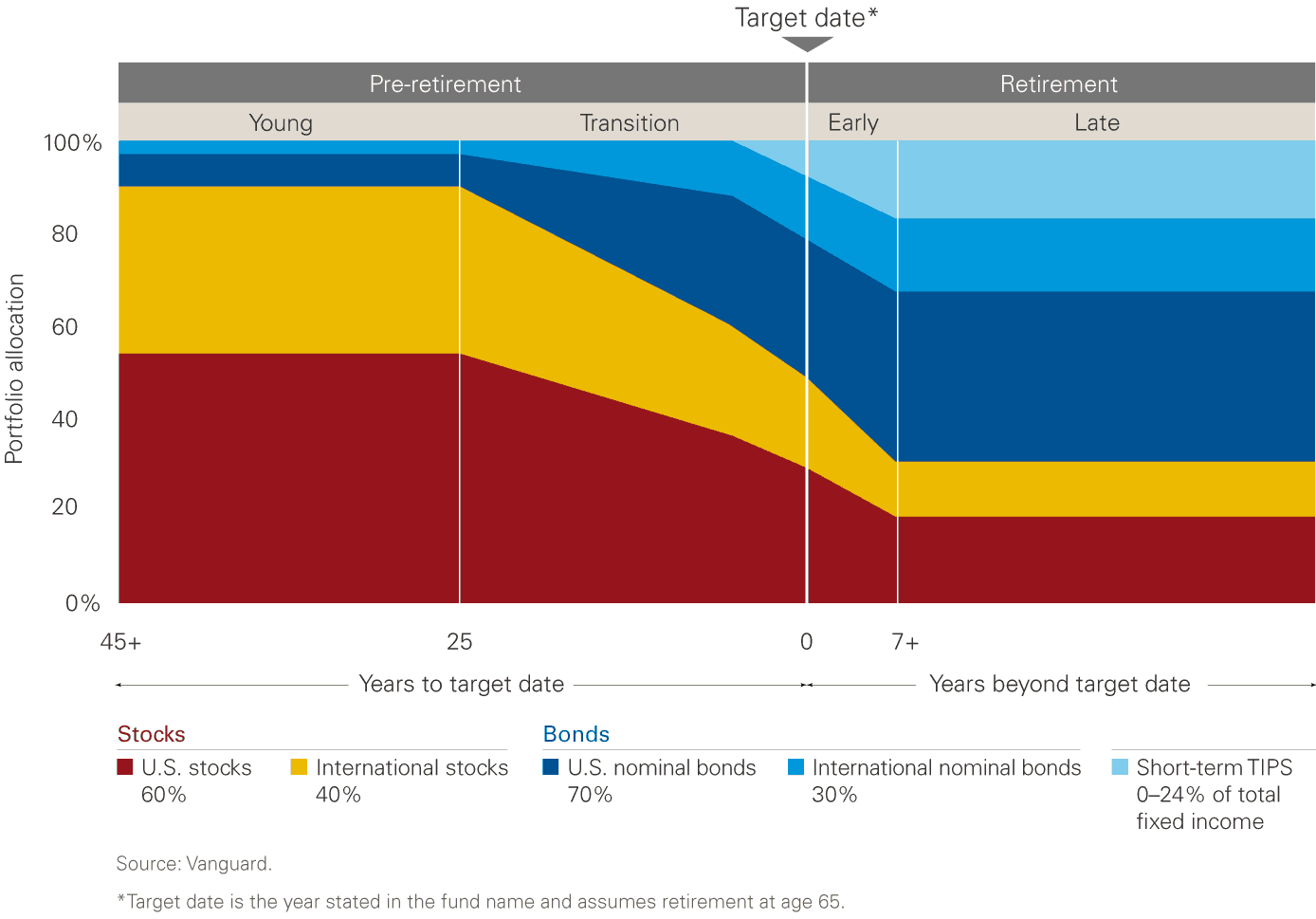

Target Date Fund Alternatives

If you don’t have the confidence to pick your investments, you can let a fund manager do it for you.

Every major broker has its version of a target retirement fund – which adjusts based on your target retirement date. The names may be different, but the goal is the same. Vanguard calls them Target Retirement Funds, Fidelity calls them Freedom Funds, Charles Schwab calls them Target Date Funds, etc.

These options are also going to be slightly cheaper on fees and be easier to manage because these funds of funds are themselves just a single fund. For tax purposes, it’s a single line item and not the underlying list.

Whereas target-date funds adjust to glide towards a “retirement date,” you can also just pick based on your desired allocation. Vanguard offers LifeStrategy Funds that are simple mixes of stocks and bonds, each with a recommended time horizon:

- LifeStrategy Income Fund: 80% bonds, 20% stocks for an investment horizon of 3-5 years, 0.11% fee

- LifeStrategy Conservative Growth Fund: 60% bonds, 40% stocks for an investment horizon of 5+ years, 0.12% fee

- LifeStrategy Moderate Growth Fund: 40% bonds, 60% stocks for an investment horizon of 5+ years, 0.13% fee

- LifeStrategy Growth Fund (VASGX): 20% bonds, 80% stocks for an investment horizon of 5+ years, 0.14% fee

These funds hold other Vanguard funds. For example, the LifeStrategy Growth Fund (VASGX) holds these Vanguard funds (as of 10/31/2021):

- Vanguard Total Stock Market Index Fund Investor Shares – 49.00%

- Vanguard Total International Stock Index Fund Investor Shares – 32.00%

- Vanguard Total Bond Market II Index Fund – 13.30% (institutional only)

- Vanguard Total International Bond Index Fund – 5.00%

- Vanguard Total International Bond II Index Fund – 0.70%

But unlike robo-advisors, if you sell your shares of VASGX, you only report the sale of VASGX and not the four underlying funds.

You don’t have to keep track of four funds, just the one.

Underlying Strategy Changes

When you invest with a robo-advisor, you rely on the robots and their designers.

Sometimes robots change.

In February of 2018, Wealthfront introduced its in-house risk parity fund, Wealthfront Risk Parity Fund (WFRPX). As a default, 20% of everyone’s investment went into their in-house fund. You could opt out, but you had to explicitly opt out rather than explicitly opt in.

Naturally, some people didn’t like that (I wouldn’t).

Risk parity itself is not new, it is an allocation strategy based on risk (volatility) rather than assets and expected returns (if you want to build your own, use Portfolio Visualizer and select Risk Parity from the Optimization Goal dropdown).

It’s a fine strategy but it’s not the same as what most robo-advisors originally promised – asset allocations relying on low-cost index funds. That hasn’t gone unnoticed.

What also didn’t help was that this fund underperformed and people were not happy, as often is the case when something loses money. It also changes the nature of the business, from an allocation advisory service to one that also has a fund… and steering people to that fund.

That’s a single case, for now, but it highlights an important concept – when you rely on another person to make decisions, you have to accept the outcomes too. If you give up that authority, you can’t turn around and complain when the decision has a bad result. The trouble is that if you relied on a robo-advisor so you could be hands-off, you might not want to have to watch things so closely.

When I invest in an index fund, it can also change as the index changes… but the underlying strategy won’t.

Costs & Fees Matter

Fees add up and when you’re getting something for it, it’s great. But if you reach the point where you want to do it yourself, paying a robo-advisor doesn’t make a lot of sense.

For example, most robo-advisors charge around 0.25%. Many low-cost funds charge less than 0.10%. The robo-advisor fees are on top of the underlying fund costs too, so with a robo-advisor you would be paying 0.35% compared to 0.10%.

Over decades and on a portfolio of hundreds of thousands or a million dollars, the fees become significant.

If you start with $1 and save $100 a month for 30 years and both appreciate at 7% a year (compounded monthly):

- The investment with a 0.35% fee would be worth $113,904.86

- The investment with a 0.10% fee would be worth $119,624.91

- The investment with a 0.00% fee would be worth $122,005.22

It’s a difference of $5,720.05, which doesn’t seem like a lot over thirty years, but that’s about 5% in gains you’re losing to fees.

And to make matters slightly worse, sometimes a robo-advisor may require you to hold a percentage of your investments in cash… and they charge fees on that too. That money is not earning 7% a year but at some robo-advisors it does get a competitive return to savings, which helps mitigate this.

Many Don’t Offer a Plan

There’s more to financial planning than asset allocation, tax-loss harvesting, and the more tactical aspects of investing.

Wealthfront has tried to address this with their financial planning tools, which focus on homeownership, retirement, travel (sabbatical type travel), and college.

But there’s something about sitting down with someone and talking through your future plans and capturing the whole piece. This is not something a robo-advisor would be able to do with algorithms. This is fine when you’re early in your investing career when your goals are very clear-cut – I want to buy a house at age X, I want to retire at age Y, etc.

But once you start getting a little more complicated with a lot more inputs, it may be better to pay a fee-only financial planner to help you chart out an actual plan. You can start by going the do-it-yourself route and create your financial plan, then speak with a professional to give it a look.

Plus, there’s value in being able to talk to a human being about your finances.

Final Thoughts

I think robo-advisors are a great innovation. They’ve helped a lot of people save a lot of money and invest it in a very intelligent way.

They’re also very inexpensive for the service they provide, with fees around 0.25%, and that’s far less than what actively managed mutual funds charge (~1%).

If you’re new to investing, they’re worth a look. If you’re more of a DIY-type of person, I think you’re better off investing the time to read some good investing books and going the index fund route, as long as it doesn’t keep you on the sidelines for too long.

Here are the robo-advisor reviews on Wallet Hacks:

And remember, the key to investing is to get invested early and often.

Hey Jim – Have you ever compared the above Betterment and Personal Capital portfolios to a simple 3 – 5 fund lazy portfolio using the visualizer? When I did this after meeting with several advisors or reviewing a published advisor, (Ric Edelman), selections, the advisors always have performed worst after fees. I can never understand why they use such complicated portfolios, especially with newer investors. It scares and confuses the hell out of them. Like the author,JL Collins, said, “1) you can learn to select an advisor, or 2) you can learn to invest.” Both take time, however #1 is… Read more »

The fees are always what get you because low cost funds are so inexpensive – it’s hard to compete with 0.04%!

I think all those complicated portfolios are complicated because they have to justify fees. If I charged you 1% (or even just 0.25%) and said – take 80% total market, 20% total bond – you’d leave in a heartbeat. You need the laundry list to seem “worth it” even though the laundry list isn’t objectively better. It’s just objectively more complicated.

As always, great article Jim! I’m with you in that I would never invest via a robo-advisor, heck, I barely feel comfortable investing with a real person! In my small circle of friends, I have heard way too many people losing their hard earned money to unscrupulous financial advice. Therefore starting small, and taking the small ding sometimes is all part of the learning process. But now, investing for myself is quite enjoyable, and most times profitable..ha!

The best dings to take are when you’re starting and things are small!

I heartily agree with the points you made in this post. The most important being that target date funds are much simpler and that sometimes people (especially once they have significant assets) may need to talk to a (fee-only) professional to think through their own goals and tax situation. This stuff gets complicated pretty quickly with real people and significant assets.

Thanks Jim for the article.

I found this white paper that Vanguard published: https://www.vanguard.com/pdf/ISGQVAA.pdf

Vanguard – of all firms – published this white paper that found working with an advisor can add 3% (bottom of page 4) in net returns! I believe this is the second version of this research. Thought I’d share. I do think Robo Advisors have helped drive down fees which is great. Most individuals aren’t as smart and savvy as you and need someone to help them. And if someone has tax issues to deal with, an advisor can really add value.

I’ve invested a small amount with Betterment just to see how it works. I’ve made small contributions over several years in what is considered a high-risk portfolio. My annual returns have averaged 5.6% (using my calculations theirs). This return seems to be on the low side, given the risk. It’s considerably lower than my other investments. I love Betterment’s interface and agree that it may be useful for those getting started. I also agree that it’s not that hard to invest on your own with just a simple portfolio. Thanks for letting me know that I’m not alone in my… Read more »

That is low given a “high-risk” portfolio… I think I’d be disappointed but it’s all in what they selected for high risk. High risk doesn’t always mean high return!

Hi Jim, Good article, I would mention that robo-advisors may be good simply for tax accounts and no one should use them for tax deferred considering that they offer no benefit. You cannot tax loss harvest in a tax advantaged account and a target date fund will do just fine, at a lower cost. Fidelity and Vanguard essentially offer a three or four fund portfolio that rebalances for you, so I don’t see any reason to go with a robo advisor there, however for someone looking for a tax efficient set and forget sort of situation, it might work out… Read more »