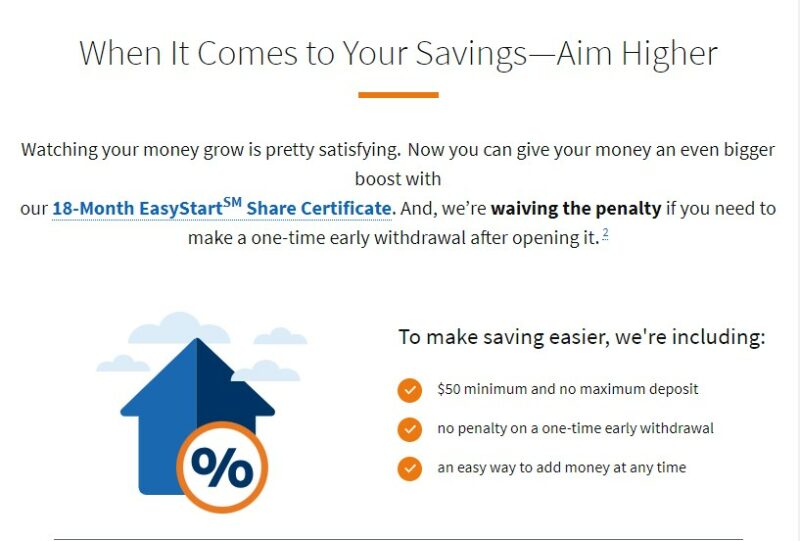

Reader Mike sent me an intriguing certificate of deposit offer from Navy Federal Credit Union – their Limited-Time Offer: 18-Month EasyStart Share Certificate. It's a no-penalty add-on CD with an 18-month term, coupling two features I've never seen together (yet).

I have no relationship with Navy Federal Credit Union, so I can't speak to the experience of using their CDs, but Mike did and said that he previously had an add-on CD that worked well:

But, I have one from a similar offer they made last year. It was a 15-month add-on CD (not a no penalty CD), APY was 5.0% and I have made a small deposit every month since I opened it.

Here's why I find it interesting:

- It's a no-penalty CD – 7 days after opening, you can make one full or partial withdrawal from the CD without paying a penalty.

- It's an add-on CD – you can add money to the CD at any time during the term.

The current yield on the CD is 4.70% APY, which is less than the highest no penalty CD rates and high yield savings account rates. The rate is a bit lower for that flexibility but it's still better than what you'd get for a traditional CD at your local brick and mortar bank.

Banking products are becoming more flexible

It seems there's a trend towards banking products becoming more flexible.

Before smartphones and online banks, you had a checking account, savings account, and certificate of deposits. You could only transact six times on a savings account or face penalties. Your checking account was meant for transactions and paid you no interest. Everything else was “savings,” and even then, the interest was terrible. CDs were strict – you could only deposit money once and were penalized heavily for withdrawing your money before the CD matured.

Nowadays, it seems like it's all getting mixed together, especially if you are working with an online bank. Checking accounts pay interest, though savings and CDs pay more. And they've even suspended the 6 ACH rule, so you can have as many transfers as you want between savings and checking.

Finally, you have all kinds of CDs – no-penalty, add-on, no-penalty add-on, bump-up, etc. And with online banking, it's become even easier to open up a CD. You don't have to visit a branch and talk to a teller or banker, you can do it completely online or through the app.

This latest offer from Navy Federal Credit Union exemplifies this trend towards flexibility. Now you can get a CD that you can withdraw from without penalty and add to it whenever you want.

Is this the future?

Personally, it's probably a response to how easy it is to open a CD.

The CD has a minimum of $50 so if you really wanted flexibility, you can open multiple small CDs and then Navy Federal has to deal with all the paperwork (probably computerized anyway but still). The add-on feature is less amazing when you realize you can just keep opening more CDs. In this case, you know what the rate is and in a falling rate environment, that can be a benefit.

I think that these types of CDs are similar to bump-up CDs, where in a rising rate environment you can bump up the interest rate of a CD to the prevailing rate. They exist in part because customers have such low friction in changing products.

In the past, you had to visit a branch and transact in person. It's way faster now.

Am I really going to waste an hour going to the bank to get 0.10% APY higher? No way.

Will I spend 5 minutes on my phone while I'm waiting around? Sure.

I'm eager to see if this trend becomes the norm.

What do you think about these?

A great hedge if short term interest rates decline below 4.70% during the next 18 months.

It has a lot of flexibility, too bad it’s not just a little bit higher rate!

Just buy vmfxx. Good enough money market rate and you can add or withdraw anytime you like. Current yield is 5.39%.

That’s true, also the current high rate for a high yield savings account is 5.55% too.